You appear to be using an older verion of Internet Explorer. For the best experience please upgrade your IE version or switch to a another web browser.

When we talk about inequality, we are talking about nothing less than the basic structure and history of modern society--the ways in which markets distribute rewards and resources, the ways in which policy corrects or compensates for market failures, and the ways in which both markets and politics shape the experiences and prospects of individuals and of families. Understanding inequality, in this respect, is not just about grasping the dimensions, or the change over time, in the metrics of inequality; it is about the trajectory of modern American political history, and the policies and policy retreats that brought us to this point.

The full meaning and importance of American inequality rests on three observations. First, American inequality is exceptional. By any measure, we are more unequal now than we have ever been, and we are more unequal—by a long shot—than our peers among developed and democratic nations. Second, contemporary American inequality is purposeful. American inequality is not an unhappy consequence of unrelenting market and historical forces; it is a direct and tangible result of public policies whose very design and intent was to redistribute income and wealth upwards. Third, American inequality is consequential. American inequality hurts not only those that it leaves behind, but does great damage to our more general economic and democratic prospects.

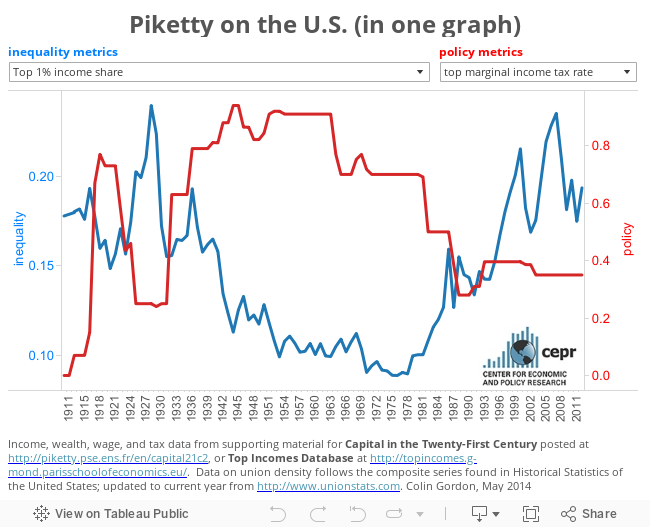

The dimensions and causes of that inequality are fully described and explained in the pages that follow. The graphics below offer a summary overview. The first distills the basic findings (for the U.S.) of Thomas Piketty's Capital in the Twenty-First Century: the now-familiar “suspension bridge” of income inequality, dampened only by the exceptional economic and political circumstances of the decades surrounding World War II; the growing share of recent income gains going to the very high earners (the 1% or .01%); the stark inequality within labor income (see the top 1% and top 10% wage shares) generated by the emergence of lavishly-compensated “supermanagers”; and a concentration of wealth that fell little over the first half of the twentieth century and has grown steadily since then.

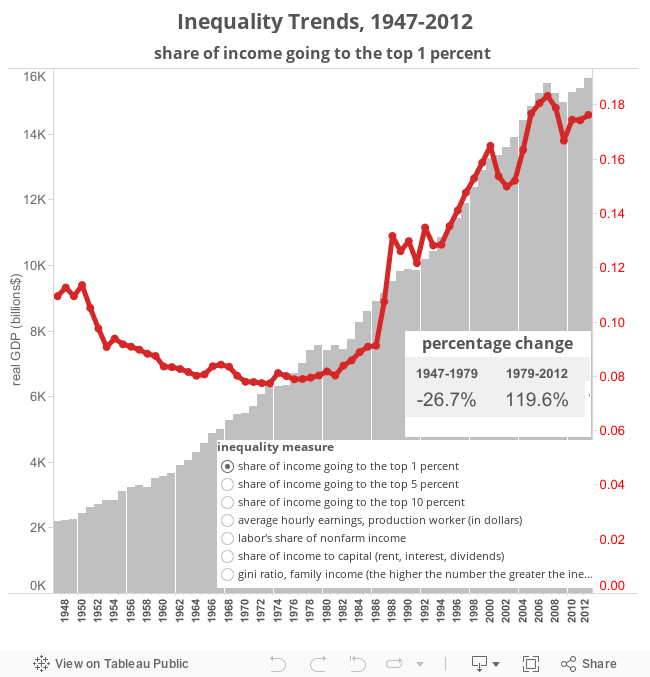

The second graphic (below) zeros in on inequality measures and metrics since the end of the Second World War, highlighting the sharp break in the late 1970s. The basic pattern is not hard to discern: against a backdrop of fairly steady economic growth (the grey bars show gross domestic product in inflation-adjusted 2012 dollars), the richest Americans have raced ahead. Working Americans and their families, by contrast, are either treading water or slowly sinking.

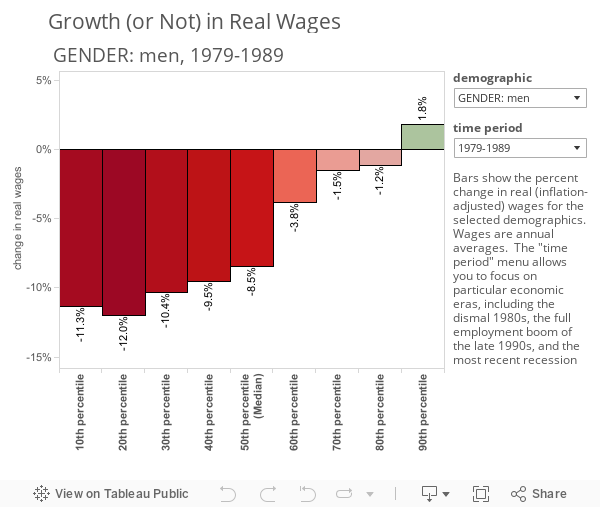

The dimensions of that inequality are both familiar and depressing. A smaller share of national income is flowing to wages and earnings, and—more important—inequality within that labor share is widening. As a result, wage growth has flatlined for a generation [see graphic below]. Middle-income workers make no more now than they did in the late 1970s; those in the lower wage cohort have lost ground over that span [click here for more on wage inequality and its sources]. The current inequality of labor income in the United States, as Thomas Piketty concludes, "is probably higher than than in any other society at any time in the past, anywhere in the world, including societies in which skill disparities were extremely large."

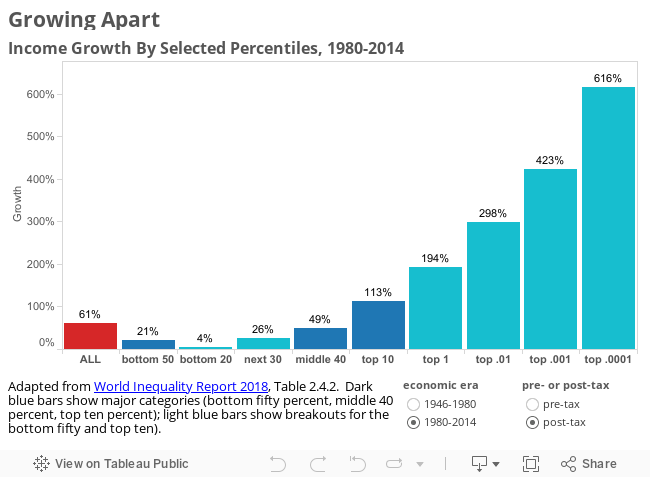

The growing gap in income (including non-wage income like returns on investment or capital gains) is even starker. In the first generation after World War II (through the end of the 1970s) income gains were evenly distributed, and the bottom 50 percent of earners actually out gained the top 10 percent. Since 1980, that shared prosperity has collapsed: Between 1980 and 2014, the pre-tax income of the bottom 20 percent fell by 25 percent, while the top .0001 percent say their earnings swell by over 600 percent. Between 1979 and 2007 alone, the real incomes of the richest .01 percent almost tripled, while the real incomes of the median household inched up only about 17 percent—and that almost all due to an increase in labor force participation and hours worked [click here for more in income inequality and its sources].

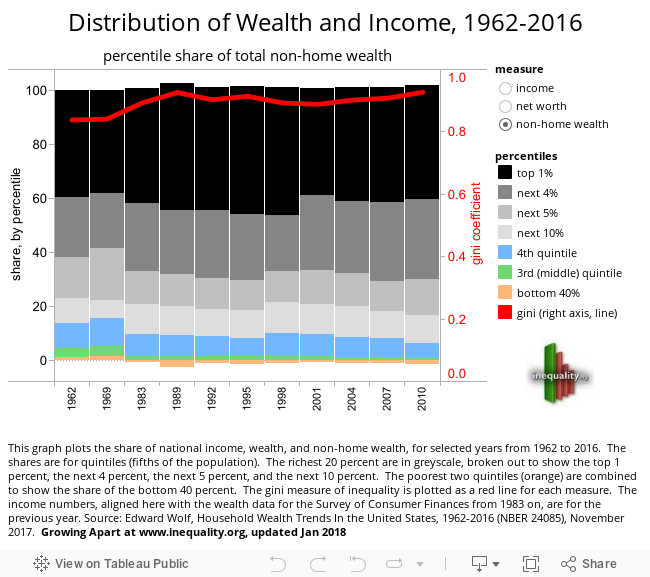

Inequality in wealth (the sum total of household savings, home equity, investments, and debts) is starker still [see graphic below]. The richest 1 percent claims over a third of the nation’s wealth; the top 5 percent claim over 60 percent [click here for more on wealth inequality]. These shares have grown steadily over the last generation. The recession took a big bite out of middle-class wealth (much of which is vested in home equity). And the gains of the recovery have flowed almost exclusively to the richest Americans.

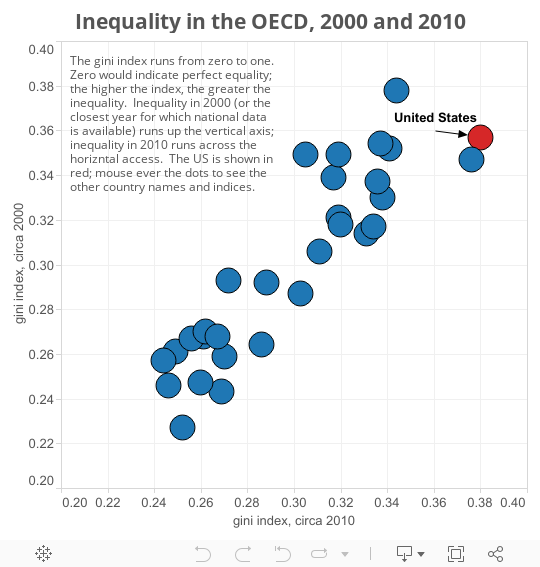

On each of these fronts, inequality has grown more in the United States than it has elsewhere. Nowhere in the industrialized world is there a bigger gap between wage growth and productivity growth over the last two business cycles. Over the last twenty years, the richest Americans started with a bigger share of income than any of their well-heeled peers and gained more than any of them. Among the world’s wealthy countries (those with an average adult wealth of $100,000 or more), the U.S. ranks dead last on the relevant inequality measures. The graphics below plots the gini index measure of inequality for 2000 and 2010 for the United States and its OECD (Organization for Economic Cooperation and Development) peers. By this measure, the United States is second only to Portugal in 2000, and--its inequality growing at a faster rate than that of any of is peers, an unqualified number one by 2010.

To make matters worse, demography and geography widen those gaps for many Americans. The gender gap in wages, income, and wealth has closed very slowly [for more details], and much of that progress is driven by the collapse of male wages rather than real gains by working women. The racial gap in wages, incomes, and wealth has closed little [for more details], and it has widened for those caught up in the startling (and racialized) spike in incarceration in the United States. While racial segregation in our cities has abated somewhat over the last generation, economic segregation—the likelihood that Americans live in enclaves of wealth or poverty—has hardened [for more details]. Economic mobility, by any measure, remains weak [for more details]; the recent spike in inequality has simply hardened that dismal American admonition: “choose your parents wisely.”

For all the jaw-dropping comparisons—between rich and poor, between then and now, between the United States and other nations—we lack a clear and compelling account of how and why we arrived this point. Our current economic troubles have aimed a spotlight at our inequality problem, but they did not create it.

What did? Conventional explanations generally posit one or both of two plot lines. The first: somebody took the money. This version stresses Wall Street greed and the Bush-era tax cuts and features a plutocracy determined to claim more than its share of private wealth and shoulder less than its share of public goods. The second: something happened to the economy. This version has a backstory in the inexorable march of globalization and technological change, and a more recent plot twist: the recession that began in 2007 and—for most of us—has not yet ended.

These accounts are not so much wrong as they are misleadingly incomplete, inattentive to longer-term historical trends and to the political choices made across that history. A fuller explanation starts to come into focus when we consider the political and economic conditions that prevailed right after the Second World War. At that historical moment, the United States displayed much narrower gaps between the rich and poor than we do now. The gains of economic growth back then were much more broadly distributed. And working families (at least white working families) enjoyed much greater economic security.

This was no accident or lucky combination of circumstances. It was the outcome of political struggle and policy choices that erected a foundation and a structure for shared prosperity. The inequality of the twentieth century’s early years actually began closing before economic growth took off in the 1940s, as a consequence of the political response to the Great Depression. Thanks to this response, federal support for collective bargaining rights sustained a surge in labor organization that dramatically improving the bargaining power of America’s workers. Other political innovations of the New Deal—ranging from Social Security to the minimum wage—secured a floor for working-class incomes. Postwar social movements, especially civil rights and second-wave feminism, then girded that floor by closing off avenues for discrimination.

The nation’s tax system, meanwhile, and new regulatory obstacles to speculative finance erected something of a ceiling for higher incomes. And substantial public investments—the GI Bill support for access to higher education, mortgage subsidies for veterans, housing projects, the interstate highway system, and the Cold War—kept the rest of the structure in pretty good repair.

Since then, that structure has essentially collapsed. This collapse is often recounted as an unfortunate but necessary response to changing economic conditions: the world has become a leaner, meaner, more competitive place. As a result, the policies of the New Deal—and the costs they imposed on business—had to go. But there is little evidence to actually support this account. Indeed, the initial hand-wringing over American economic decline came at a time when our principal competitors, Japan and Germany, boasted both higher wages and more expansive social programs than the United States.

Political choices, not economic necessity, dismantled the New Deal. Future Supreme Court Justice Lewis Powell would first sketch out the organizational and ideological dimensions of these choices in a now infamous 1971 memorandum to the U.S. Chamber of Commerce [for the details]. The conservative ascendance in state and national politics affirmed these choices across the political landscape, with dramatic consequences: steep cuts in social spending, the political abandonment of organized labor, deregulation and privatization, tax cuts, punitive cycles of unemployment—all justified in the name of lowering business costs, capturing economic efficiencies, and unleashing markets. Such arguments, of course, camouflaged the real goal of the pushback against the New Deal: a redistribution of income upward via the erosion of the hard-earned bargaining power of ordinary Americans. Rising inequality was not a lamentable side effect of America’s new policy framework; it was its intent.

Why Does it Matter?

Such inequality, in the view of many economists, is not just the toll we pay for free markets, but an essential incentive within a market economy. People work hard to avoid poverty and even harder to get rich. Any pursuit of "equal outcomes" would stifle this initiative and, with it, the economic growth on which we all depend. The poor, as they like to say, will find themselves much better off with a thin slice of a growing pie than with a thicker slice of a small one.

There is little evidence—historical or economic—to substantiate such silliness. The “market incentives” argument holds water only as long as hard work is reliably rewarded in the short term (with wages) and in the long term (with economic mobility)—a prospect that has unraveled in the last decade. The economy does not need inequality to grow. In fact, nearly the reverse is true. In our own recent history, sustained economic growth is closely associated with a relatively equitable distribution of economic rewards. Even the International Monetary Fund has conceded on this point, concluding recently that “lower net inequality is robustly correlated with faster and more durable growth.”

Stark and sustained inequality discourages those at the bottom of the income distribution ladder (whose hard work goes unrewarded), and encourages those at the top to engage in short-sighted speculation—much of which (think predatory lending and usurious credit card rates) exploits the poor and widens the gap. Inequality matters, most obviously and directly, to those whom it leaves behind. This includes the very poor—the “underclass” or “the truly disadvantaged,” in the social science literature—who have long been cordoned off from the rewards and opportunities enjoyed by most Americans, but also the broad middle class, for whom growing inequality has begun to erode wealth, incomes, living standards, and opportunities.

Inequality also matters more generally, to society at large and to the health and prosperity of all who live within it. The evidence on this point is overwhelming. Citizens in unequal societies, researchers have shown, are more likely end up sick, obese, unhappy, unsafe, or in jail. These social outcomes, bad in themselves, also undercut the productivity and efficiency of the economy, as the high costs of poor public health, heavy policing, and mass incarceration siphon off our resources and leave our human capital underprepared and underutilized [more on the costs of inequality].

More directly, at a certain point, stark income gaps begin to hollow out consumption. “A millionaire cannot wear 10,000 pairs of $10 shoes,” as one advertiser warned on the eve of the Great Depression in 1929, “but a hundred thousand others can if they’ve got the $10 to pay for them, and the leisure to show them off.” Rising inequality in the last generation has created the same tension, eased only temporarily by the availability of consumer credit and home equity. Such efforts to patch together substitutes for aggregate demand create their own inefficiencies—including a bloated and parasitic financial services sector, fed by both the desperate demand for credit from those falling behind and the frantic search for speculative returns by those leaping ahead.

Finally, economic inequality endangers democracy. Market power will always shape political outcomes, if only because the rich will always have both the wherewithal and the motive to play a role more influential than any individual votes they might cast. But pervasive or sustained inequality has broader political consequences. Massive inequality tends to tilt public policy toward shortsighted rewards or special treatment (deregulation, tax breaks) and away from the public or collective goods (education, infrastructure) essential to future economic growth. Economic inequality breeds inequality in politics, whose highest goal, in turn, becomes policies that make economic inequality even worse.

Democratic institutions, at their best, provide a basic physical, legal, and fiscal infrastructure in which markets can thrive. These institutions can ameliorate or regulate the excesses of market competition and provide the public goods and services that markets are unable or unwilling to generate on their own. Under conditions of stark economic and political inequality, all of this begins to unravel. Shortsighted and speculative market activities get rewarded, not restrained. Collective investment in the economy’s infrastructure—everything from good schools to good roads—withers. And deepening economic inequality robs our politics of the collective will—and the resources--to do much about it.14

A Road Map to These Pages

This introduction lays out the basic dimensions of American inequality. For more detail or background, follow the "CLICK HERE" links (in the text above, and replicated here) to further explore the trajectory of American wages (the compensation paid directly to workers on an hourly or salaried basis), incomes (which includes non-wage forms of income like return on investment or capital gains, and it groups individuals into families, households, or tax units), and wealth (savings, home equity, and investments); demographic (race and gender), spatial and generational patterns of inequality; and the costs of inequality.

First and foremost, the chapters that follow seek to lay out the political and institutional changes which have contributed to the stark rise of inequality in the last generation.

The next section, Usual Suspects, critically assessed the various explanations most commonly advanced to account for our inequality, particularly those that lean on broad and immutable trends in global competition, technological change, or family structure.

This clears the deck for Differences that Matter, where we trace the key policies--or policy reversals--that have brought us to our current unequal state of affairs. Here we both explain what has changed and assess—drawing on the relevant economics literature—how and when and to what degree each policy shift contributed to inequality.

By way of conclusion, our final section touches on possible and promising solutions.

Discussion of "Introduction"

Add your voice to this discussion.

Checking your signed in status ...