Blue Collar Mortgages

One of the simplest and starkest measures of growing inequality lies in the juxtaposition of blue collar earnings with costs of sustaining a middle-class standard of living. Wages for most Americans and incomes for most American families have slipped or stagnated for a generation. Core household costs (for education, for health care, for transportation) have, over the same span, continued to rise.

Housing is especially important in this respect, because it is both a household expense and, as an investment, a source of household or intergenerational wealth. The graphic below summarizes income or earnings, and housing costs, for a few key demographics . The green bars, rising sharply between 1970 and 1980 and then leveling off, show the monthly payment (assuming a loan at 90 percent of value on prevailing terms) on a median value home. The 1960-1980 spike in housing costs, in this sense, reflects both steadily rising home values, and high interests rates. The blue bars show monthly income or earnings. And the table in the lower left shows the share of monthly income or earnings (depending on the chosen demographic) needed to make those housing payments.

The takeaway is clear. For starters, there is a stark racial gap. At the point in the 1950s and 1960s when housing was most affordable for white working class men, their incomes were nearly double those of black men. In the 1950s and 1960s, housing costs ran at about one-fifth the median monthly income of a white male, or the average monthly earnings of a production worker (shown here are earnings for production workers in all manufacturing, durable goods manufacturing, automobiles, and meatpacking).

Over the next decade, things changed dramatically: incomes and earnings withered, housing costs continued to rise, and housing terms deteriorated. By 1980, housing costs claimed half of the average earnings in manufacturing –a little more than that in industries, like meatpacking, where the move to a low-wage, largely non-union workforce came earlier; a little less in industries, like automobiles, where union presence hung on.

The second graph (below) captures, with annual data, the trajectory of blue collar earnings from the late 1940s to the present. The pattern, over all, is a familiar one. Average earnings in manufacturing (shown here are a few core sectors) rise in a brisk and parallel fashion from the end of World War II through the late 1970s. From 1945-1978, average earnings for production workers almost double (up 95 percent). From 1978-2012, they flatten out—falling 2.3 percent over that 34 year span. The trajectory varies by industry—as they are exposed to trade, concessionary bargaining, and other wage pressures in different ways and at different times. But they all lose ground to housing costs (the thick grey line), which continue to climb steadily.

Housing is especially important in this respect, because it is both a household expense and, as an investment, a source of household or intergenerational wealth. The graphic below summarizes income or earnings, and housing costs, for a few key demographics . The green bars, rising sharply between 1970 and 1980 and then leveling off, show the monthly payment (assuming a loan at 90 percent of value on prevailing terms) on a median value home. The 1960-1980 spike in housing costs, in this sense, reflects both steadily rising home values, and high interests rates. The blue bars show monthly income or earnings. And the table in the lower left shows the share of monthly income or earnings (depending on the chosen demographic) needed to make those housing payments.

The takeaway is clear. For starters, there is a stark racial gap. At the point in the 1950s and 1960s when housing was most affordable for white working class men, their incomes were nearly double those of black men. In the 1950s and 1960s, housing costs ran at about one-fifth the median monthly income of a white male, or the average monthly earnings of a production worker (shown here are earnings for production workers in all manufacturing, durable goods manufacturing, automobiles, and meatpacking).

Over the next decade, things changed dramatically: incomes and earnings withered, housing costs continued to rise, and housing terms deteriorated. By 1980, housing costs claimed half of the average earnings in manufacturing –a little more than that in industries, like meatpacking, where the move to a low-wage, largely non-union workforce came earlier; a little less in industries, like automobiles, where union presence hung on.

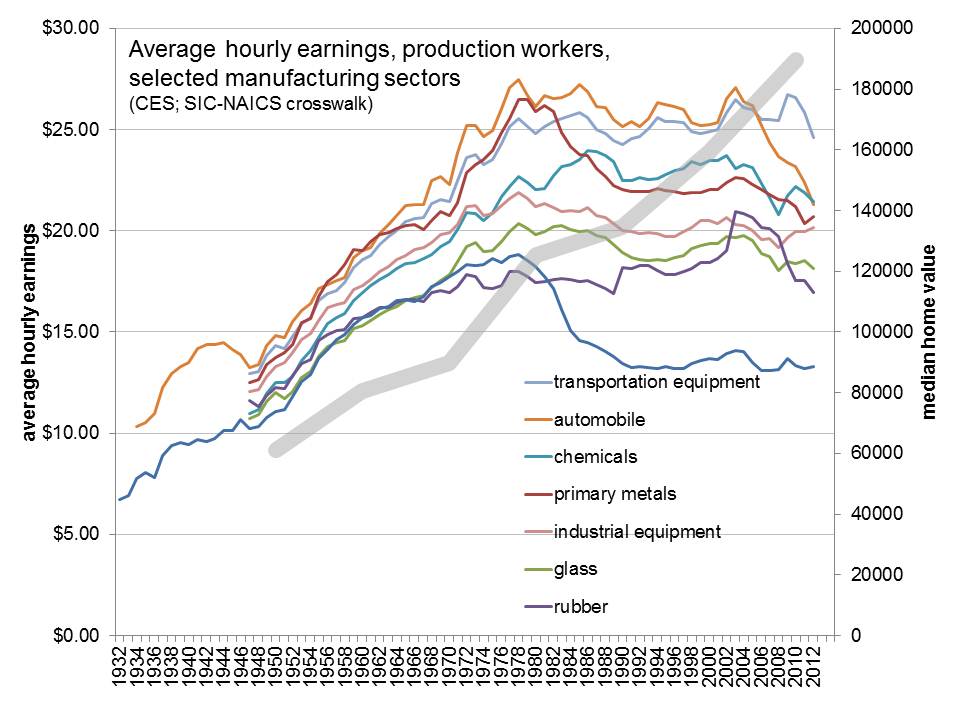

The second graph (below) captures, with annual data, the trajectory of blue collar earnings from the late 1940s to the present. The pattern, over all, is a familiar one. Average earnings in manufacturing (shown here are a few core sectors) rise in a brisk and parallel fashion from the end of World War II through the late 1970s. From 1945-1978, average earnings for production workers almost double (up 95 percent). From 1978-2012, they flatten out—falling 2.3 percent over that 34 year span. The trajectory varies by industry—as they are exposed to trade, concessionary bargaining, and other wage pressures in different ways and at different times. But they all lose ground to housing costs (the thick grey line), which continue to climb steadily.

{kind=link}

Discussion of "Blue Collar Mortgages"

Add your voice to this discussion.

Checking your signed in status ...