Book Review: Examining Macroeconomic Policies in the Global South

By Shalin Hai-Jew, Kansas State University

{kind=link}

Macroeconomic Policies in the Countries of the Global South

Anis Chowdhury and Vladimir Popov, Editors

New York: Nova Science Publishers

2019

344 pp.

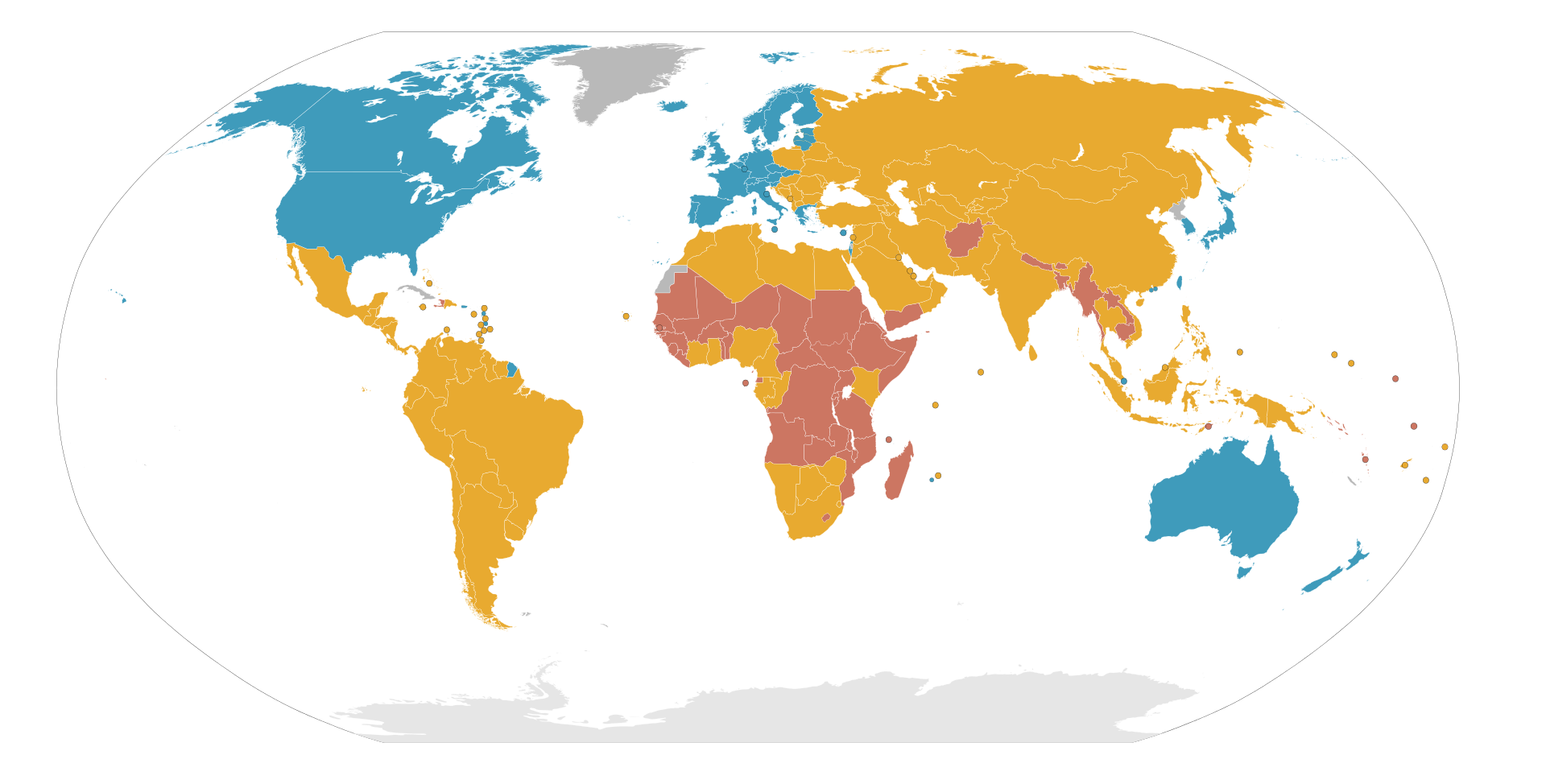

Anis Chowdhury and Vladimir Popov’s Macroeconomic Policies in the Countries of the Global South (2019) offers insight into the thinking behind and practices of macroeconomic policy-setting in some of the regions of the Global South, a swath of countries that include lower-income and middle-income countries. In the map, the countries depicted in yellow and red are part of the Global South, broadly speaking. (Figure 1) This book focuses on macro-economic policies “conducive to inclusive and sustainable growth in developing countries” (Chowdhury & Popov, 2019, p. vii). In other words, what policies will enable the countries of the Global South to lower poverty and include the very poor in work while ensuring that the economy continues to grow at a rate that may be sustained (without the extremes of booms and busts), and moving towards the consensus-built sustainable development goals (SDG) of the United Nations? The works apparently stem from the 2017 – 2019 research project at the Dialogue of Civilizations Research Institute in Berlin and a culminating workshop “Macroeconomic Policies in Countries of the Global South,” which occurred on Nov. 15, 2018.

The respective works touch on fiscal and monetary policies, the management of foreign direct investment, the role of central bank independence in monetary policies, and economic objectives—which must include the well-being of the poorest and most vulnerable in society.

{kind=link}

Figure 1. Least-to-Most Developed Countries in 2008 (IMF) (by Spacepotato)

{kind=link}

National Economies 101

A national economy may be conceptually modeled as an idealized system. There is the country’s governing system, with its executive, its laws, its enforcement mechanisms, its cultures, its practices, and its staffs, among other levers of power. There is its taxation system, how moneys are taken in, managed, and distributed. There is its finance system, which affects which efforts are funded and how and moneys repaid. There is its moneys, and how its value is backed up through a central bank and its policies (especially setting its lending rate to other banks). There are a nation’s public expenditures and how it spends its moneys. There are the relationships with other governments and the treaties a government engages in and the military actions and wars it enters into. A national economy is a critical part of national security because it affects the intelligence agencies it can deploy, the type of defense that may be put up, the type of military personnel and technologies it can field, the backing it can offer its diplomatic staff (carrots and sticks that can be offered), the strength of its universities, the developed talents of its peoples, and other factors.

In an idealized sense, a well-run economy is one in which a population is fully employed (and unemployment is low), money retains its value over time / prices of goods are stable (low inflation), interest rates are sufficiently high to encourage savings but are sufficiently low to encourage spending (particularly on durable goods), the gross domestic product (GDP or the value of all final goods and services in a country for a particular time period, not counting those products and services in the black market) is at optimal levels for the particular society, trade with other countries is mutually beneficial and generally “fair” with a shared set of standards and laws and practices, taxation is sufficient for government services and not excessive, and the needs of society are generally met. Ideally, information is accurate, markets are generally transparent, people play by the rules and are on the up-and-up, and there are no major unnecessary disruptions.

A healthy economy is expected to grow over time, with more mature ones slowing down in its growth as a percentage of the overall economy. (The elderly and sick are cared for, the young are educated, and so on.) The study of “macroeconomics” involves the study of the entire economy, based on various aggregate statistics and federal policies. At the macro level, economies may go through expansions and contractions, booms and busts. Industry verticals rise and fall; they change in what looks like slow motion and with many indicators (2020 hindsight), but on the ground, in the lived sense, the pressures may feel enormous and threatening. The micro decisions made by individuals individually and socially may cause various forms of emergence of larger-scale outcomes.

An economy can be sensitive to policies, which can directly affect the health and productivity of various sectors, with “winners” and “losers” in the colloquial sense, and which can ultimately affect the economy’s productivity, its speeding up/slowing down, and people’s lived sense of opportunities for work, for pay, for benefits, and for the types of work available. In a theoretical sense, given the basics of a country, there can be an idealized achieved economy that optimizes all resources for optimal outputs, but limits to leadership, human health, natural disasters, and other challenges mean a lesser achievement.

In terms of national economic accounting, various indices are collected by the respective governments and reported out. These indices may suggest the relative health of the economy, whether it is expanding, peaking, contracting, or in a trough part of the cycle. The accuracy of the data is critical, and ideally, there is only one set of books that the government uses and also shared with the world.

Lessons Learned about Macroeconomics in the Global South

Anis Chowdhury and Vladimir Popov’s “Introduction: Major Observations” (Ch. 1) opens with six key lessons learned from macroeconomics in the Global South. Insufficient investments into “public goods such as education, healthcare, infrastructure, law and order, and administration” can result in “a collapse of output,” such as in the 1990s in post-communist countries. If taxes are not progressive (rich pay more, transfer payments made to the lowest quintiles), then greater social inequalities will arise (higher Gini coefficients). They note: “Low inflation policy tends to suppress output growth, and in developing countries with relatively high per capita income, central bank independence can contribute to lower inflation, but at the expense of growth.” Next: “Countries with flexible monetary policy manage adverse supply shocks better, especially if wage and price rigidities exist.” “Exchange rate undervaluation through the accumulation of foreign exchange reserves promotes export-oriented growth in developing countries because exports-to-GDP ratios in these countries are generally below optimal levels.” (Chowdhury & Popov, 2019, pp. 1 – 2)

And finally: “Macroeconomic policies need to be nuanced, instead of ‘one-size-fits-all’, to suit country-specific circumstances.” (Chowdhury & Popov, 2019, p. 2) The challenge seems to be to understand the various strengths and weaknesses of each particular country in its respective stage of development and the optimal “settings” for each of the policies. Of course, idealized statistical models are fairly tidy, within the limits of available data, but the world itself is comparatively dynamic and messy. What are the political systems and leadership goals? How ready are populations for various changes? How adaptable are the educational systems? What does the work infrastructure look like, and how well does it handle employment churn? How much does the respective country engage with others in the world, and how, and how well integrated is it? What are its orientations? What is each country getting right, and what is each country getting wrong? What is difficult about mass-scale transitions, and how can these challenges be mitigated?

The authors observe various tradeoffs. A country that is inward-oriented tends to become “inefficient and burdened with rent-seeking activities, (while) some outward-oriented economies became more vulnerable to external shocks and financial crises” (Chowdhury & Popov, 2019, p. 2). Developing countries, even with fewer resources, are not inured to the world—changes in global rules (that nations can opt into), shifts in oil costs, shifts in commodity values, changes in trade rules. The slowdown in economic growth in Global South countries in the 1980s was partially blamed on “the failure of the Washington Consensus macroeconomic policy framework” and on “the quality of institutions prevailing in the countries where these policies were implemented” (p. 4). [The core issue seems to have been whether governments should take on more debt and spend more to create economic growth, or if they should pull back on spending and control for high debt levels.] They write:

In general, from all points of view, the dynamics of government expenditure during transition seem to have been far more important a factor in successful transformation than the speed of reforms. Keeping the government big does not guarantee favourable output dynamics, since government spending has to be efficient as well. However, the sharp decline in government spending, especially for the ‘ordinary government’, is a sure recipe for the collapse of institutions and a fall in output, accompanied by growing social inequalities and populist policies. (Chowdhury & Popov, 2019, p. 6)

When real government expenditure falls by half or more from a previous spending level, governments become unable to enforce laws effectively to fight crime and enforce contracts and ensure social order. (China is called out as an anomaly here. Even though the government pulled back from some expenditures, it was still able to maintain economic growth.)

The co-authors make some close-in observations of developing countries:

For many developing countries with rigid prices and wages, moderate inflation is often caused by cost push factors, i.e., adverse supply shocks. Hence, inflation-targeting in these countries often needs an excessively tight policy putting constraints on output growth.It looks like the negative relationship between inflation and growth effectively only exists when inflation exceeds several dozen percent a year. But if inflation runs at a level of 20 – 25% or below, the relationship between growth and inflation becomes positive, as shown by a normal Phillips curve: a negative relationship between inflation and unemployment. The theoretical foundations for this non-linear link have been extensively studied in the literature since Bruno and Easterly’s 1996 paper, and the presence of these non-linearities in transition economies is documented in numerous papers. (Chowdhury & Popov, 2019, p. 7)

Developing countries with limited foreign exchange reserves may deal with “negative terms of trade or financial shocks” by maintaining “a fixed exchange rate, or even a currency board, and wait until the reduction of foreign exchange reserves leads to a reduction in the money supply” (monetary contraction) which should “drive domestic prices down and stimulate exports, raise interest rates, and stimulate the inflow of capital, and finally correct the balance of payments” or devalue its own national currency (Chowdhury & Popov, 2019, pp. 8-9) to achieve the prior. The devaluation of a national currency was found to have less of an effect on outputs than the first (Chowdhury & Popov, 2019, p. 9). To promote export-oriented development, some economies will undervalue their own currency and accumulate foreign exchange reserves as a macroeconomic policy and industrial policy. The co-authors suggest that the prior policy moves would fail if all countries applied them but suggest that developing countries should be allowed to use such policy levers for “catch-up development” (Chowdhury & Popov, 2019, pp. 12 - 13). [Developed economies cry foul, since such policies by developing countries can result in the “dumping” of particular goods into their economies and undercut their industries.]

New Developmental Macroeconomics for Middle-Income Countries

Luiz Carlos Bresser-Pereira’s “The Rise of a New Developmental Macroeconomics for Middle-Income Countries: From Classical to New Developmentalism” (Ch. 2) tracks the change in thinking from classical to a new developmentalism.

This work begins with some definitions: What is “development economics” in the North is “structuralism” in Latin America and called “classical developmentalism” here. Developmentalism is “a form of economic and political organisation of capitalism that differs from economic liberalism” (Bresser-Pereira, 2019, p. 23). A core idea involves sparking periods of faster economic growth in order to grow one’s way out of unemployment. Classical developmentalism “defends moderate but strategic state intervention in the economy, not only because there are non-competitive sectors in the national economies of even rich countries, but also because savings are insufficient and markets in pre-industrial countries are poorly developed, poorly regulated, and not sufficiently ensured by the state” (Bresser-Pereira, 2019, p. 25). A main strategy in this approach was the “important substitution strategy” enabled through setting high import tariffs on manufactured goods so that domestic manufacturers can provide those same goods, creating domestic jobs serving domestic markets; the domestic markets could be extended through integrations with other regions who could also provide consumers for those manufactured goods (Bresser-Pereira, 2019, p. 25)

In the 1980s, with the confluence of the advent of Marxist “dependency theory” and a global debt crisis, researchers found that extant research did not fully anticipate the real-world challenges and contradictions, with profits being captured in developed economies and less so in the periphery of the developing ones. “New developmentalism” is a theoretical framework “that explains both growth and growth failure in developing countries, particularly Latin American middle-income countries that suffer from the Dutch disease and from dependency in relation to the North” (Bresser-Pereira, 2019, p. 29) [“Dutch disease” is defined as “the apparent causal relationship between the increase in the economic development of a specific sector…and a decline in other sectors” (“Dutch disease,” Nov. 11, 2019). The mechanism is thought to be the contribution of the developing sector’s success to the rising value of the national currency, which raises the cost of exports and diminishes markets for other goods.]

The author coined the term “new developmentalism” initially in 2003 “to underline its theoretical difference in relation to classical developmentalism and its rejection of populist or vulgar developmentalism” and followed with a paper in 2006 (Bresser-Pereira, 2019, p. 30). In ensuing years, this concept was defined with suggested actions to enable developing countries to competitively integrate with international markets in strategic and tactical ways (p. 35), without experiencing many of the externalities related to economic interactions with developed countries. (The nuances of the framework are too complex to effectively summarize here.)

Public Expenditure and Progressive Taxation

Anis Chowdhury’s “Fiscal Policy for Inclusive Sustainable Development: The Role of Public Expenditure and Progressive Taxation” (Ch. 3) suggests a focus on the re-distributive power of government expenditures and expansive fiscal policy (based on Keynesian economics). Conventional thinking by the World Bank and International Monetary Fund had for decades suggested that economic stability would lead to both economic growth and inclusion (of the poor) in the economic benefits of societies. Where prior goals were focused on lowering fiscal deficits—with the assumption that private expenditures would possibly substitute for lowered public ones—empirical analysis suggests that the latter did not materialize in any significant way. Corporate tax cuts were not found to result in increased corporate investments in public goods (Chowdhury, “Fiscal Policy…,” 2019, p. 43). Newer thinking, in the aftermath of the 2008-2009 global financial crisis (GFC), suggests that fiscal policy can be somewhat more activist to distribute economic resources more fairly throughout a society, with less disparity between the rich and the poor. Specifically, the author asserts that countries of the Global South “should examine the growth and distributional impacts of the size and composition of public expenditure and revenue-raising mechanisms to balance stabilisation and development goals…and build-up their fiscal space to be able to consistently pursue inclusive, growth-oriented counter-cyclical fiscal policy” to expand expenditures in times of downturn and recession and contract when the economy is overheating (Chowdhury, “Fiscal Policy…,” 2019, p. 44), to balance against economic cycles.

The historical leeriness of taking on government debt (deficit financing) is seen as a restriction to inclusive and sustainable development. This work embraces Keynesian macroeconomics for developing countries and apparently stands against belt-tightening and austerity approaches to fiscal management. This work does also suggest that different ideas and practices popularize at different times, and individual thinkers may be lauded in certain time periods over others.

External loans given to developing countries have often come with the strings of required reforms and particular microeconomic policies, with the idea that these fiscally disciplined practices (“the critical importance of macroeconomic stability and the need for using numerical fiscal targets in guiding fiscal policy”) would “spur growth and reduce poverty in low and middle-income countries” (Chowdhury, “Fiscal Policy…,” 2019, pp. 46 - 47). Over the years, there have been various and changing narratives around this issue. There have been the advancing of various fiscal rules representing “legislated and long-term numerical limits on budgetary aggregates pertaining to debts, deficits, expenditures, and revenues” (Chowdhury, “Fiscal Policy…,” 2019, pp. 47 - 48). The idea is that rules can restrain over-spending in the good times and enable savings for the downturns. In developing countries, often, taxation is pro-cyclical and is not as helpful during business downturns (pp. 50 – 53). The author makes the point that developing countries experience “fiscal risks due to privatization and public-private partnerships” due to the profit-seeking motives of private industries (pp. 53 - 54). Given the focus on inclusive development, orthodox economic ideas may not be as applicable. This author writes: “If the fiscal deficits-inflation-external balance relations are not as straight-forward as the orthodoxy believes, then one cannot make any confident assertions about the link between debts and macroeconomic instability” …or to “high public debt…to lower growth” (Chowdhury, “Fiscal Policy…,” 2019, p. 62), suggesting that there is space for more public debt in the developing world than global lenders might suggest. Are fiscal rules created by an “independent fiscal agency” too restrictive, and maybe even threatening of “democracy and development”? (p. 67)

Enabling Inclusive Sustainable Development

Anis Chowdhury’s “Creating Fiscal Space for Inclusive Sustainable Development” (Ch. 4) opens with a UN estimation that “several trillion dollars per year would be needed annually for climate-compatible and sustainable development, with U(S)$5-7 trillion of additional financing for infrastructure” (p. 87). How governments collect taxes, finance their endeavors, service debt obligations, and spend public moneys are critical parts of promoting sustainable development. Developing countries have lower tax-GDP ratios and have tighter fiscal spaces in which to function because of a larger informal economy, less efficient tax administration, a smaller tax base, and other challenges. In this work, the author describes various common and “innovative” taxes that may be collected to advance the work. In the latter category are “environmental taxes,” “resource rents” (p. 99), sin taxes, and financial transactions tax (p. 100). Corruption, tax avoidance and evasion, and other challenges may hinder the full collection of taxes. Alternative sources of revenue may include private savings (p. 104). Public-private partnerships, while lauded by some global organizations, are seen as shifting too much risk to the private sector and too little to the private (p. 105), as too expensive (p. 106), not particularly effective in terms of development outcomes like “poverty reduction and inclusive development,” and potentially distortive of priorities (pp. 106 – 107).

The author writes:

Illustrative simulations at the IMF (Baum et al., 2017) reveal that the fiscal space available in low-income countries will be insufficient to undertake the spending needed to achieve the SDGs, even under benign conditions. Traditional approaches, such as improving public investment efficiency and domestic revenue mobilization, can somewhat narrow the gap, but will still fall far short of what is required. They cannot avoid resorting to deficit financing through borrowing from the banking sector. (Chowdhury, “Creating Fiscal Space…,” 2019, p. 110)

Inclusive Fiscal Policy and Tax Administration

Donghyun Park’s “Inclusive Fiscal Policy and Tax Administration Effectiveness in Asia” (Ch. 5) begins with the advancement of Asian countries economically. In 1990, “more than nine out of ten Asians lived in a low-income country,” but by 2015, “more than nineteen out of twenty Asians lived in a middle-income country,” according to the Asian Development Outlook. (Park, “Inclusive Fiscal Policy…,” 2019, p. 116) Advancing from a middle-income status to a high-income one is thought to be much more challenging based on the Latin American experience. A main challenge remains that of maintaining a cleaner environment while advancing human economics and living standards. The Asian region has seen increasing inequality in the same period given “globalisation, technological progress, and market-oriented reform” (p. 117). Governments’ ability to both tax and spend, in their fiscal policy, may be the difference, particularly for children and the elderly (and other groups potentially left behind). In Asia, private transfers of moneys within families to children play a more important role than in Europe, where public transfers are more salient (p. 119). Public transfers for the elderly are “noticeably smaller in Asia than in Europe or Latin America” (p. 120). The author suggests space for public expenditures in education, healthcare, and other public goods.

The author argues for a standard “Tax Administration Measure of Effectiveness” (TAME) to enable comparisons of tax policies and proposes a construct in this work, based on an initial formula from 1995 (Das-Gupta, Lahiri, & Mookherjee, 1995, as cited in Park, “Inclusive Fiscal Policy…,” 2019, p. 123) and some modifications. He applies the TAME system to the numbers from various Indian states and draws conclusions about the tax administration efficacy and offers variables that may be improved. Park suggests that “periodic data collection for a TAME” may be done along with “external audits by a jurisdiction’s supreme audit institution” to improve tax administration (p. 135).

Inclusion through Government Spending and Fiscal Policy

Donghyun Park’s “Inclusive Government Spending and Unconventional Ideas for Inclusive Fiscal Policy” (Ch. 6) explores ways to reduce income inequality, such as targeted government expenditures to focus on particular income groups, including social transfers (like “welfare”), subsidized public services, education, healthcare, and other inputs. Progressive taxation is seen to have “a tangibly weaker and less direct impact on income inequality and poverty” both in developed economies and developing ones (Park, “Inclusive Government Spending…,” 2019, p. 143) but are still important since “a disproportionately heavier tax burden on the rich…(can) contribute directly to equity”.

“Inclusive growth” is defined as the following:

“...sustained, balanced, and broad-based economic growth that includes a large portion of a country’s labour force and benefits a majority of the population rather than just a small privileged elite. Inclusive growth is inconsistent with widespread unemployment or a high degree of income inequality. Inclusive growth removes constraints to growth, creates opportunity for the many, and creates a level playing field for investment…Rauniyar and Kanbur (2010) define inclusive growth as growth which disproportionately benefits those with lower incomes, leading to lower income inequality. (Park, “Inclusive Government Spending…,” 2019, p. 144)

Park summarizes the research literature on this issue of inclusive government spending and suggests that the U-shaped relationship between the “Gini coefficient and economic growth—i.e., inequality worsens as a country grows richer up to a certain income level, after which it improves” (Kuznets, 1955) seems to generally apply using Western European and Latin American data but only partially applies when East Asian country data is added. Political factors that directly aided redistribution may have interrupted that curve (Acemoglu & Robinson, 2002, as cited in Park, “Inclusive Government Spending…,” 2019, p. 145). This researcher also explores fiscal policy used to mitigate business cycle fluctuations to stabilize the economy. Generally, fiscal consolidation is seen to increase inequality. This analytical work asks whether fiscal spending “can promote equity (inclusive growth) without sacrificing economic growth” in developing Asia. (Park, “Inclusive Government Spending…,” 2019, p. 146) To actualize the research, the author constructs a cross-country panel dataset based on the Standardized World Income Inequality Database and the World Bank’s World Development Indicators. Total fiscal spending is calculated as including the following: “government final consumption expenditure; gross capital formation, public; health expenditure, public; military expenditure; social transfers and subsidies; public spending on education,” and then, the Gini market coefficient was calculated (this uses income “before taxation and transfers”) (Park, “Inclusive Government Spending…,” 2019, p. 147). Other datapoints, real GDP growth, revenue as a percentage of GDP, tax revenue as a percentage of GDP, literacy rates, unemployment rates, market capitalization as a percentage of GDP, and others, were also collected, for possible use as control variables.

Based on this data, the author conducted “a panel vector auto-regression (PVAR)” to study the effect of government spending on equity and economic growth (Park, “Inclusive Government Spending…,” 2019, p. 149) and found “gross fixed capital formation, public health spending, and education spending have significant positive effects on economic growth” with especially persistent effects from healthcare and education spending (p. 150), Both “public health spending and public education spending significantly reduce income equality in the region (p. 151). The headline of this work is that there is empirical evidence from developing countries in Asia that a government’s fiscal policy can have clear beneficial effects on both income inequality and economic growth when focused on social protections and social goods that help redistribute the benefits of a strong economy, in alignment with conventional thinking. In Asia, governments are focusing more on using fiscal policy to address issues of economic inequality (p. 156). Public investment in infrastructure, like transportation, “does not seem to have a significant direct effect on equity” but does have “a strong effect on economic growth, which is associated with poverty reduction, and thus indirectly helps to promote equity” (p. 157). The historical prudence of Asian leadership in keeping budget deficits low and public debt low gives them more leeway to make decisions even as “large fiscal demands” are anticipated given the aging populations (requiring more healthcare, social security, welfare, and other inputs). (p. 158) Park concludes by highlighting some moves that respective governments are making to reorient to the current and upcoming changes. Park also suggests that government can better support entrepreneurship and restrain corruption, to better the functioning of their economic systems.

The title of this work promised unconventional ideas, but from the outside, these ideas are only unconventional if the practices of government finance tend towards conservatism.

Setting Monetary Policy for Workable and Inclusive Development

Anis Chowdhury’s “Monetary Policy for Inclusive and Sustainable Development” (Ch. 7) examines government’s role in ensuring the amount of money in circulation, its cost to borrow, its value on international markets, and other aspects—to get the mix right for employment, consumer spending, trade (domestic, regional, and international), and other factors. Chowdhury writes: “Should monetary policy be used to minimise short-run deviation of actual output from the potential? Should monetary policy be used to stabilize the price level and other monetary variables such as exchange rates and interest rates instead of output or employment?” (Chowdhury, “Monetary Policy…,” 2019, pp. 173 - 174) Optimal monetary policy is the subject of competition based on “the complexity and uncertainty of the underlying long-run inflation-growth relationship, and…the possible short-run trade-off between price and output (employment) stabilisation” (p. 174). Early development economists suggest that “money could promote long-term growth through inflationary financing, neoclassical economists believe that money is neutral in the long run” (p. 174). This researcher suggests that monetary policy is not neutral and has “a critical role to play in promoting inclusive and sustainable development” and that moderate inflation “is not harmful for growth” or harming to the poor (He asserts: “Monetary policy is not the best tool to address food prices or supply-shock inflation.”) (p. 175). He also suggests that central banks should not just focus on single-digit inflation per tradition but have “dual mandates” of “orderly growth and reasonable price stability” (p. 175).

What follows are various cases of different countries and their experiences with central bank policies and ensuing outcomes. The author touches on fundamental questions of the effects of inflation at different levels—on wages, on prices, on the poor, on economic growth, on rent-seeking, on savings, and other factors—and reveals a diversity of opinion by different scholars. Reflecting the complexity of economic systems, there are a fair amount of “on the other hands” in the discussions. Between excessive controls and excessive liberalizations, central banks may fulfill their roles with effective and nuanced policies that better serve the citizens. [One argument is that “inflation can benefit the poor by reducing the real value of their net debt” (Chowdhury, “Monetary Policy…,” 2019, p. 186).] The author cites a research study that found that if inflation is between 5 – 15% that it did not affect the Gini coefficient in any significant way (Romer & Romer, 1999, as cited in Chowdhury, “Monetary Policy…,” 2019, p. 187).

Based on a survey of the research, the author offers six summary ideas, foremost that inflation in and of itself is not necessarily negative and that central banks should have wider mandates and wider policy levers to achieve outcomes. One point reads:

Achieve consistency with the fiscal policy stance. Safe expansionary monetary policy within the above guidelines will allow governments to borrow from the central bank to finance growth enhancing employment-intensive public infrastructure investment programmes. Private investment is unlikely to be crowded out; rather, both domestic and foreign investment will be encouraged by demand growth and the benefits of an improved physical infrastructure. This means demand growth and the benefits of an improved physical infrastructure. This means demand expansions will be matched by expansions of supply. This, well-coordinated expansionary monetary and fiscal policies can keep inflation within safe limits and promote growth and employment. (Chowdhury, “Monetary Policy…,” 2019, p. 199)

Independence of the Central Bank

Behrooz Gharleghi’s “Central Bank Independence, Inflation, and Economic Growth” (Ch. 8) engages a core tenet of macroeconomics: CBI to protect central bankers from political influence in setting policies for achieving target inflation rates. The author cites multiple studies in which central bank independence has no relationship to economic growth and one which does in both the short and long terms. To assess this question, the author used a panel regression model to examine the following: the per capita growth rate, Central Bank Independence index, level of PPP GDP per capita, interaction term, and the population growth rate, the shadow economy as a percentage of the GDP, the corruption perceptions index, and a measure of government effectiveness (Gharleghi, 2019, pp. 220 - 221). The data are collected from various datasets and varying years. The author describes mixed effects of CBI on growth in developing countries:

The first mechanism is that of monetary discipline: in countries with GDP per capita below the threshold (mostly comprised of poor countries with bad quality institutions and bad quality checks and balances), there is always a danger that the central bank will expand the money supply under pressure from the government and / or lobby interest groups. Greater central bank independence provides a kind of a blocking mechanism for this type of policy.The second mechanism is associated with price rigidities and cost-push inflation. Loose monetary policy in this case can alleviate the negative impact of price rigidities on growth by ensuring that actual output approaches potential output levels. If the central bank is too independent, it does not care about output and unemployment, but only about bringing down inflation and stabilising the exchange rates, so there is a negative impact on growth. (Gharleghi, 2019, p. 225)

In rich countries, CBI is seen as lowering growth because of tightened monetary policies (p. 226). CBI is not costless to an economy but have differing effects on developing and developed countries.

Financial Globalization and Investments

Manuel F. Montes’s “Macroeconomic Policy and Real and Financial Investment: The Impact of Financial Globalisation” (Ch. 9) suggests that when developing countries enable external agency controls over financialization and fiscal deficits, they are giving up important policy capacity over tools that may help them deal with “balance-of-payment crises…regaining and maintaining countercyclical macroeconomic policy space…harnessing resources of the financial sector to support industrial development and the creation of a productive domestic financial sector” (Montes, 2019, pp. 234 - 235). Countries that give up capital controls “is to provide a wide-open, level playing field for financial investors and companies to determine the volume and pattern of investment in the real sector” and enable them to “shape the development prospects and labour markets of all economies” (Montes, 2019, p. 235). The researcher makes the case for this view and suggests some ways for developing countries to regain power in this policy space. Montes (2019) writes:

Amongst developing countries, emerging economies have been the main destinations of international portfolio flows. However, the advice to almost all countries has been to establish an enabling environment for foreign investors. Many developing country officials have interpreted this as requiring the deregulation of capital accounts and as a policy that applies to least-developed countries (LDCs) and middle-income countries. The historical record suggests that although open capital accounts have provided periods of portfolio inflows (often followed by sudden stops and crises) for middle-income countries, foreign investment—whether of the real sector type or the portfolio type-is not often located in LDCs; rather, LDCs tend to have greater deficits in infrastructure, basic services, and political stability, which reduces their attraction for foreign investment, except in extractive sectors for specific metals and minerals. Private flows are highly unlikely to land in LDCs because of these factors; with respect to international financing, LDCs are heavily dependent on official development assistance flows. (Montes, 2019, p. 245)

The argument here is that the profit motive of corporations leaves little in the way of prosperity for developing countries and instead of creating value ends up extracting it (Montes, 2019, p. 249), in arguments that echo dependency theory. To avoid this dynamic, there is exploration of creating new asset classes of funds to help developing countries build infrastructure to be competitive and there is talk of re-regulation to change the power of foreign investors in developing countries (p. 251).

Foreign Exchange Reserves and Shocks to Short- and Long-Term Economic Growth

Vladimir Popov’s “Foreign Exchange Reserves and Exchange Rates: Reaction to Shocks in Short-Term and Long-Term Economic Growth” (Ch. 10) asks some basic questions: How should developing countries handle their foreign exchange reserves, the amount of foreign currencies that a government holds, in a way that benefits the country in the short- and long- terms? How much should it have on hand to mitigate potential shocks without excessive cost?

Countries have little in the way of reserves to deal with negative shocks, or “barely enough to withstand several months of deterioration in the terms of trade and several weeks of capital outflows” (p. 261).

The author suggests that in the short term, “it is better to manage external shocks to the capital account and the current account through changes in foreign exchange reserves, either through full sterilization—neutralising change in the money supply by selling or buying government bonds—or through fiscal sterilization, i.e., by increasing or decreasing stabilization funds (sovereign wealth funds)” to control for volatility (Popov, 2019, pp. 257 - 258). The author describes various options for a country in the face of negative shocks, with the understanding that there are tradeoffs with every set of responses. Strategically, foreign reserves “create a cushion for possible fluctuations in resource prices, but also…prevent the overvaluation of the national currency that leads to the Dutch disease” (Popov, 2019, p. 276). Real exchange rates (RERs) are generally seen as “endogenous (i.e., it cannot be influenced by government or monetary authority policies in the long run” (Popov, 2019, p. 257).

Some countries will hold a large amount of foreign exchange currencies in order to keep their value high, in order to be able to export more manufactured goods (since their own domestic currency may be kept low, so their goods are relatively lower cost and so more competitive abroad). This may ensure export markets for their domestic manufacturing.

Ambition and Pragmatism in Chinese Macroeconomic Policy

Leong H. Liew’s laudatory “China’s Macroeconomic Policy: A Policy of Ambition and Pragmatism” (Ch. 11) shows the importance of having a strategic vision around which to organize endeavors, based on a clear-eyed sense of the country’s “unique circumstances”—its “geographical location and size, its level and stage of economic development at a given point in time, and constraints imposed by regional or global economic conditions” (p. 280). His focus is particularly on the centrality of China’s “technical innovation and climate change projects” (p. 279). Liew goes on to summarize the general conditions of the PRC’s macroeconomics history and context and emphasizes their focus on “monetary autonomy” to control domestic interest rates given the criticality of the domestic (vs. export) market (Liew, 2019, p. 284). He points to the central government’s extension of “loans” (vs. subsidies) to state-owned enterprises (SOEs) as an important turning point in the country’s attempts to increase market efficiencies into their pseudo-planned economy as well as enabling companies to pursue local government financing vehicles. China’s Strategic Development Plan aligns with their One Belt, One Road (OBOR) approach to strategic security, according to Liew, and their preferential loans to those working on renewable energy and strategic technologies are part of a thought-through process (p. 288). China’s “outbound acquisitions” are comparatively low at 0.9% of GDP in 2015 (p. 289). China’s government debt (240% of GDP) is comparatively low, but their “corporate debt and the unproductive use of credit” are challenges, with highly leveraged real estate developers with excess capacity (“ghost cities”) (pp. 290 - 291). The author suggests that no macroeconomic policy is perfect, particularly when there are multiple objectives simultaneously for a government, but he extends a number of kudos to the Chinese government for their moves.

Chinese Domestic Infrastructure Investments

Justin Yifu Lin, Xinqiao Ping, and Xin Huang’s “China’s Growth-Promoting, Public-Debt-Financed Infrastructure Investment” (Ch. 12) asks: What were the effects of China’s infrastructure investments through public-debt-financed projects from 1998 – 2007, in the lead-up to the global financial crash (in 2008 – 2009)? An analysis of the data suggests the following:

A careful examination of China’s debt evolution from 1997 to 2007 reveals two phenomena worthy of attention: first, throughout that decade, the debt size (whether measured as debt issue revenue, net debt increase, or the gross government debt balance) was continually increasing, not cyclical. The debt size did not shrink during the economic growth or expansion phase; thus, debt issue was used as a countercyclical instrument à la Keynes. Second, during that decade, the debt-output ratio was stable; the central government debt ratio hovered around 15% to 19%, whereas the gross government debt ratio was below 30%; that is, the debt issue did not result in a heavy debt-repayment burden for future generations, because the debt was used for infrastructure investment. Given that good infrastructure facilitates growth, debt financing became a strategic instrument for comparative-advantage-based growth. As China’s GDP was expanding rapidly, the country’s debt ratio declined. (Lin, Ping, & Huang, 2019, p. 304)

Fundamental construction generally refers to the following: “infrastructure in agriculture, water conservancy, forestry, railroad, transportation, communications, power, and urban facilities”; “national defence, education, science, culture, health, and politics and law” and “others approved via the legislative process” (Lin, Ping, & Huang, 2019, p. 307). Only some information is publicly available about exact expenditures to particular efforts. As such, the authors use proxy statistical measures (mileage per capital, highway miles per capita) to identify peaks in public investment into infrastructure. Infrastructure investment was found to contribute directly to GDP growth, and further, it “released some bottlenecks, thereby promoting economic growth” due to lower transaction costs (Lin, Ping, & Huang, 2019, p. 324).

Conclusion

Development around the world is uneven, and the relative positioning of various countries differs. How each responds to global economic realities and their own contexts also varies, with differing appetite for risks and preferences for strategies.

This book essentially argues developing countries have different on-ground realities that they have to consider when making macroeconomic policies, and they cannot unthinkingly take on the orthodoxies and assumptions of developed countries. They suggest further that policymakers need to consider inclusion of whole populations in macreconomic decisions, in order to be inclusive. Macroeconomic decisions cannot be made in isolation from the very human impacts, with winners and losers. Respective macroeconomic ideas are advised based on particular conditionals and contexts.

Anis Chowdhury and Vladimir Popov’s Macroeconomic Policies in the Countries of the Global South (2019) opens with the sense that there are just “broad principles and tools” (p. 2) for policymakers in developing countries, and that still seems true at the conclusion of the text. The theories, models, frameworks, and data…inform decisions analyzed through differing political prisms and goals. Macroeconomics engages a complex space, and the real world limits what can be done at any one time, and it’s all relative, and it’s never ceteris paribus.

The two co-editors are long-term professionals in economics. Chowdhury “holds concurrent adjunct professorial positions at Western Sydney University and the University of New South Wales” and has consulted widely for federal banks and international organizations like the UNDP (p. 327). Popov serves as research director at the DOC Research Institute in Berlin (p. 328).

References

“Dutch disease.” (2019, Nov. 11). Wikipedia. Retrieved Nov. 18, 2019, from https://en.wikipedia.org/wiki/Dutch_disease.

About the Author

Shalin Hai-Jew works as an instructional designer at Kansas State University. Her email is shalin@ksu.edu.

Note: Thanks to Nova Science Publishers for a review copy of this text as a watermarked PDF file.

| Previous page on path | Cover, page 19 of 21 | Next page on path |

Discussion of "Book Review: Examining Macroeconomic Policies in the Global South"

Add your voice to this discussion.

Checking your signed in status ...